2026 Insurance Investment Outlook: Challenges warrant a defensive posture

nvestment opportunities certainly still exist for insurers, but valuations and mixed economic signals call for a defensive posture, in our view.

Gain investment clarity in Asia Pacific through our research, specialized insights, and thought leadership.

This newsletter brings the latest topics impacting insurers, aimed to help those managing investment portfolios while considering an insurer’s business, regulatory and solvency needs.

For the first edition of our Invesco Insurance Insights for 2026, we illustrate the approach used to assess a hypothetical strategic asset allocation (SAA). We consider how updated return expectations for various asset classes could impact the portfolio’s expected return, whether the portfolio is still positioned appropriately, and assess how a careful selection of other asset classes can help make the portfolio more efficient.

As always, please do not hesitate to reach out to us – your thoughts on such topics are much appreciated.

Jaijit Kumar, Head of Asia Insurance Solutions

Hello everyone, welcome to our first edition of the Invesco Insurance Insights newsletter for the year. Here, we’re illustrating the process of a periodic review of an asset allocation. The main elements we consider are – how have these assumptions and expectations changed and their impacts on the existing allocation, and what adjustments can we consider that could enhance these portfolios.

While insurance portfolios tend to be designed for the long-term, it remains important to assess them frequently to ensure they are still fit-for-purpose and are still positioned to deliver the desired results. In this example, we start with a generic asset allocation - representing a base portfolio. We have allocations to government bonds to manage duration, some credit exposure for yield enhancement, and listed equities and real estate to provide potential upside opportunities. And we assess the expected return and certain risk-based charges for this portfolio – and especially how these may have changed year-over-year based on updated assumptions.

We then assess the impact of adding certain asset classes – to see if we can improve key metrics. In our updated portfolio, we’ve incorporated small allocations to private credit, value-add real estate, and private equity – as examples - looking to extract some premium, and to help further diversify the portfolio. The results are then assessed and additional changes can be made if required – this is meant to be an iterative process.

It remains important to have a deep and thorough understanding of such new asset classes – as these can potentially introduce new sources of risks – so, it remains vital to ensure that portfolio parameters remain well managed and contained under various stress scenarios.

As always, we hope that this topic will be of benefit to you in your on-going assessment, construction, and management of portfolios, and we’ll be more than happy to discuss any of these aspects further.

Thank you.

In this edition of insurance insights newsletter, we’re illustrating the process of a periodic review of an asset allocation. The main elements we consider are – how have these assumptions and expectations changed and their impacts on the existing allocation, and what adjustments can we consider that could enhance these portfolios. Watch the video to learn more.

Hello everyone, welcome to our first edition of the Invesco Insurance Insights newsletter for the year. Here, we’re illustrating the process of a periodic review of an asset allocation. The main elements we consider are – how have these assumptions and expectations changed and their impacts on the existing allocation, and what adjustments can we consider that could enhance these portfolios.

While insurance portfolios tend to be designed for the long-term, it remains important to assess them frequently to ensure they are still fit-for-purpose and are still positioned to deliver the desired results. In this example, we start with a generic asset allocation - representing a base portfolio. We have allocations to government bonds to manage duration, some credit exposure for yield enhancement, and listed equities and real estate to provide potential upside opportunities. And we assess the expected return and certain risk-based charges for this portfolio – and especially how these may have changed year-over-year based on updated assumptions.

We then assess the impact of adding certain asset classes – to see if we can improve key metrics. In our updated portfolio, we’ve incorporated small allocations to private credit, value-add real estate, and private equity – as examples - looking to extract some premium, and to help further diversify the portfolio. The results are then assessed and additional changes can be made if required – this is meant to be an iterative process.

It remains important to have a deep and thorough understanding of such new asset classes – as these can potentially introduce new sources of risks – so, it remains vital to ensure that portfolio parameters remain well managed and contained under various stress scenarios.

As always, we hope that this topic will be of benefit to you in your on-going assessment, construction, and management of portfolios, and we’ll be more than happy to discuss any of these aspects further.

Thank you.

Jaijit Kumar, Head of Asia Insurance Solutions illustrates how insurers can potentially enhance their portfolios using updated capital market assumptions. He then shows how private market assets can be incorporated into an insurer’s portfolio to modify the risk-return profile, using the examples of private credit, value-add real estate, and large leveraged buyouts.

nvestment opportunities certainly still exist for insurers, but valuations and mixed economic signals call for a defensive posture, in our view.

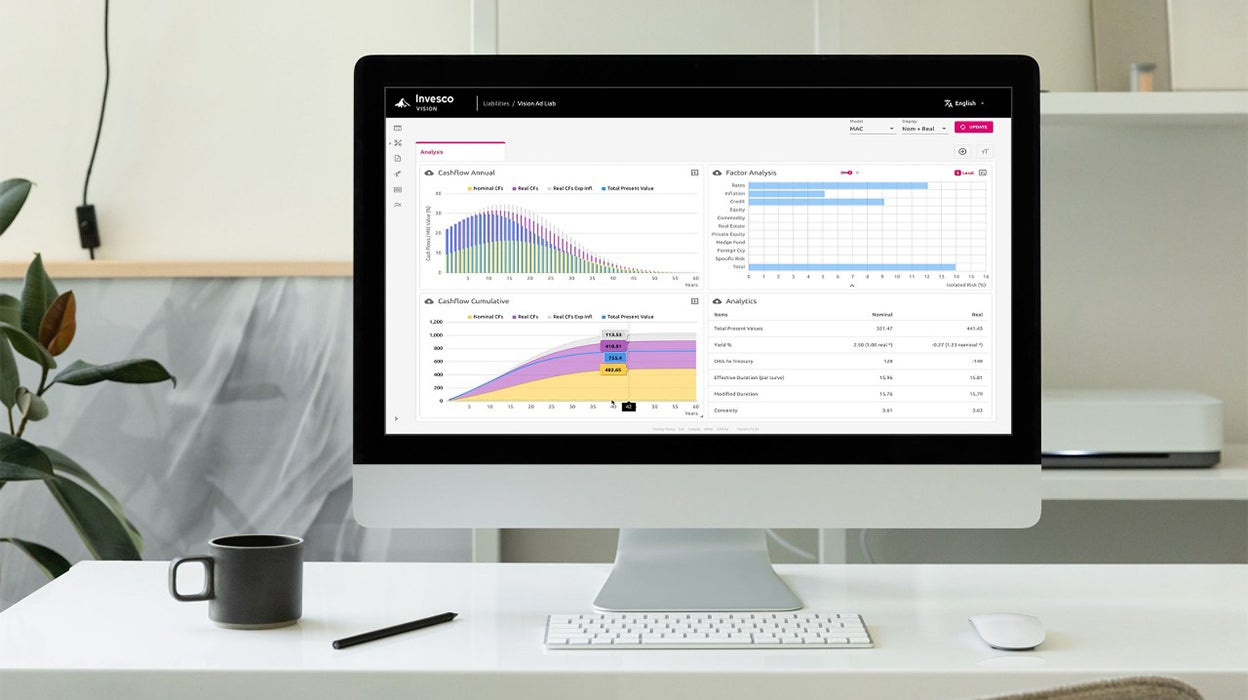

This newsletter explores a bottom-up approach to fixed income portfolio efficiency. Leveraging our proprietary analytics platform, Invesco Vision, we demonstrate how insurers can build more resilient and optimized portfolios.

Jaijit Kumar, Invesco’s Head of Asia Insurance Solutions shares his Q2 2025 case study on adopting a multi-alternatives strategy to enhance insurer’s portfolios.

Thomas Wu and David Chao in Invesco’s Global Strategy and Insights team, explore how global markets have remained resilient amid geopolitical tensions, shifting US tariff policies, and energy market volatility, highlighting why strengthening fundamentals still support a more positive global growth outlook for 2026.

CLOs could offer the potential to align with certain needs of insurance portfolios, primarily around diversification and yield enhancement, opening up possibilities of tailored asset strategies and risk/return profiles.

In episode 2 of the Institutional Conversations Podcast, our private credit and ETF specialists discuss why private credit has recently made headlines for the wrong reasons and what is driving the growing interest in AAA CLOs.

The Vision platform is a state-of-the art, portfolio diagnostics tool to “pre-experience” how different variables affect investment outcomes. By identifying risk and return drivers, including under certain risk-based capital regimes, as well as exposures to an array of factors, Vision effectively characterizes the inherent risks in a defined liability or cash flow profile to identify optimal investment strategies.

Request a demonstration of the complimentary portfolio management research and analytics service.