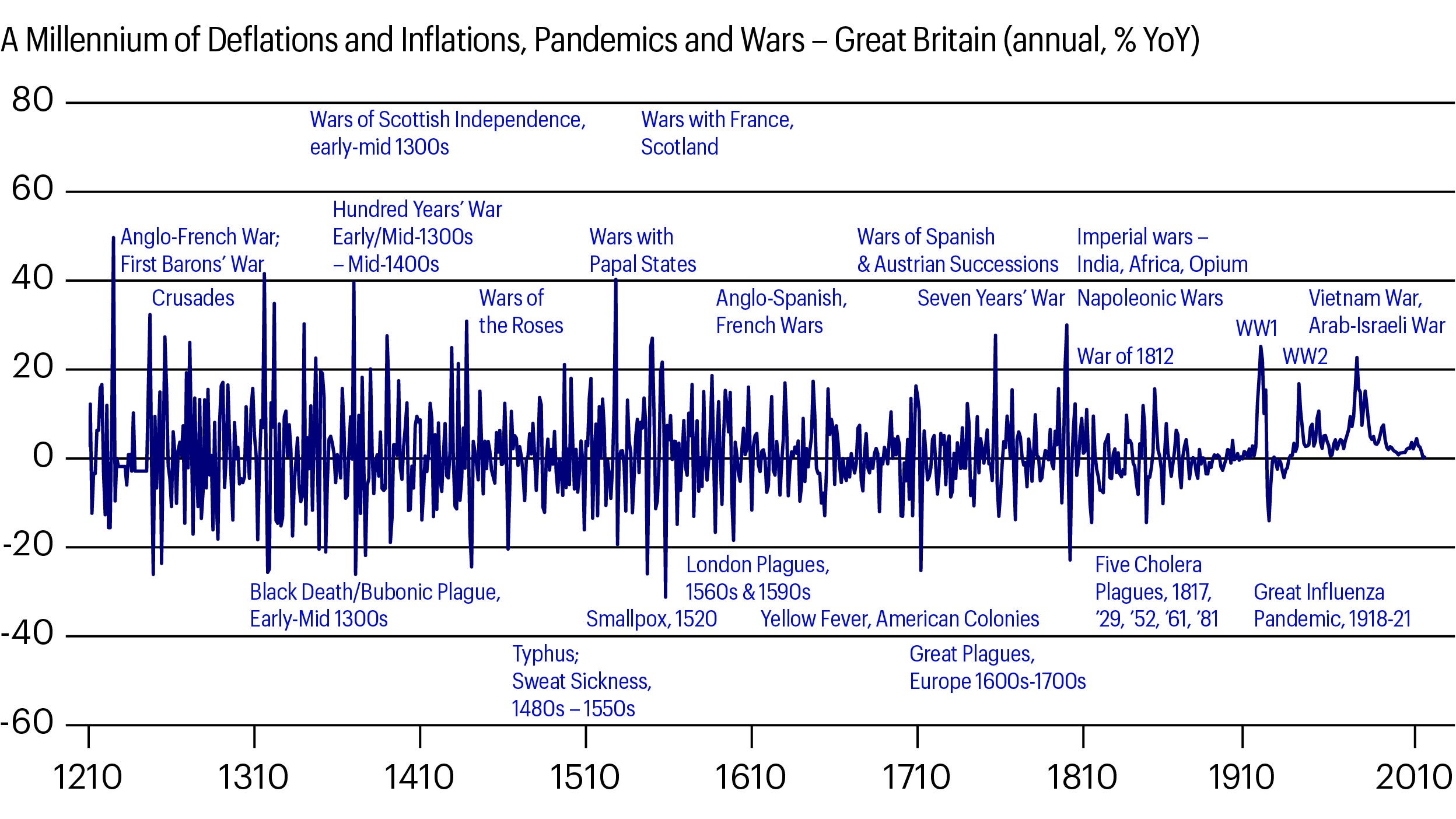

This isn’t to say that the world of today is the same as the world of the last millennium – clearly, the global economy, public health systems, fiscal, monetary and financial systems are all completely different than they were in the distant past. Nor is it to say that deflations always owe to pandemics (or inflations to wars). Yet, pandemics have generally been deflationary and wars, almost always inflationary.

Still, pandemics throughout history have required social distancing and lockdowns. Severe past pandemics caused proportionally far more deaths than COVID-19, and therefore resulted in more demand destruction and deflation – largely because health systems and science were much less advanced, and because there was far less fiscal or monetary support in past episodes.

The British experience of pandemics may well offer a rough and ready guide. Pandemics destroy demand (usually, faster and more extensively than they damage supply), whereas wars boost demand, through mobilization and fiscal stimulus – often with inflationary, monetary financing – as they destroy supply.

Two other themes also come through. Inflation has shown enormous volatility over time, with few sustained trends2. Inflation volatility was lower in the 20th century than before, with fewer major pandemics or wars. But those that did occur were accompanied by severe deflations and inflations. This suggests that the right policies can cope with deflationary or inflationary shocks, reducing macroeconomic volatility and providing a more stable decision-making environment for firms and households, and thereby improving financial backdrop for investing in risky ventures and risk assets.

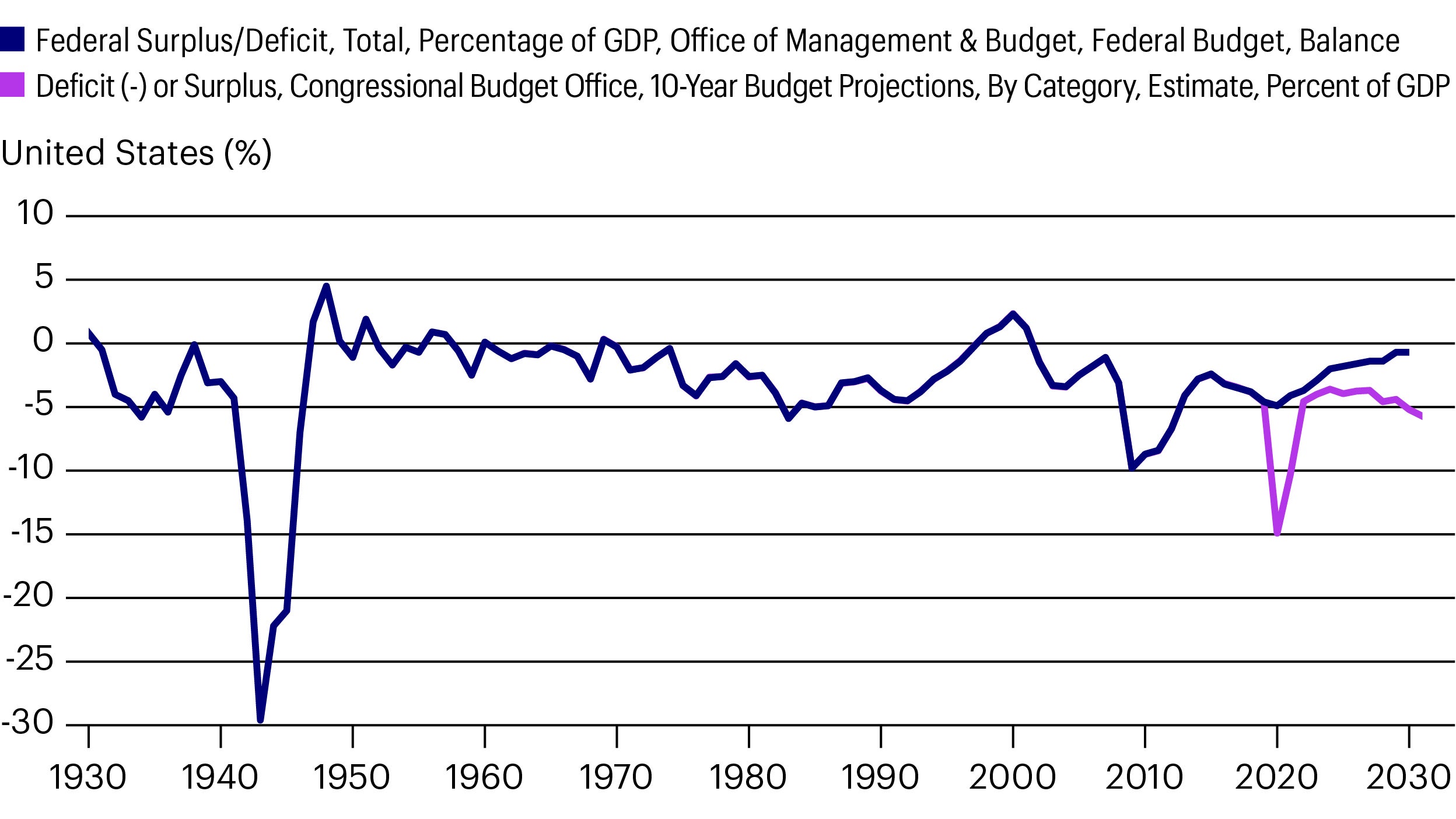

This pandemic is clearly going to be different. Deflation is already being avoided, thanks to monetary easing and fiscal transfers and guarantees, preventing collapses in economic activity, financial markets as well as employment and the activity of firms. But even in the US, where concern is strongest about inflation, fiscal support is unprecedented in peacetime. However, official estimates remain below the scale of major wars.